With the next RBA decision due on June 16 and markets still reacting to the Budget and Middle East conflict, many borrowers are reassessing their position. Here are four issues worth watching:

- What the Budget changes could mean for investors

- How borrowers are coping with higher rates

- Refinancing activity jumps as rates rise

- New fund aims to unlock housing supply

Tax Changes Could Reshape Property Investing

The federal Budget has proposed major changes to negative gearing and capital gains tax – and property investors are now reassessing their plans.

From 1 July 2027, negative gearing for residential property would largely be limited to new builds. At the same time, the current 50% capital gains tax (CGT) discount would be replaced with a system based on inflation indexation and a new 30% minimum tax on capital gains.

Why current investors may avoid major changes

Importantly, existing investment properties held before 12 May 2026 would be exempt from the negative gearing changes.

That means many current investors may see little immediate impact.

But for future buyers, the picture could change significantly.

Why new builds matter more now

The Budget papers make it clear the government wants to encourage investment into newly constructed housing. Investors who purchase eligible new builds would still be able to access negative gearing and choose between the current CGT discount or the new indexed approach.

That could shift more investor demand toward:

- Off-the-plan apartments.

- House-and-land packages.

- Duplex and townhouse developments.

Why investors are reassessing strategy

There’s still uncertainty around how the reforms will play out.

But regardless of the final outcome, the conversation around investment property strategy has clearly changed.

If you’re thinking about buying, refinancing or restructuring an investment loan, we can help you understand how these proposed changes could affect your borrowing strategy and long-term plans.

Borrowers Adjust To Higher Rates

Three rate rises in four months are now hitting household budgets – and many borrowers are reassessing their next move.

Most lenders have already passed on the Reserve Bank’s May cash rate increase to variable-rate borrowers, although some changes are still filtering through.

That means many households are now feeling the combined impact of the February, March and May rate rises all at once.

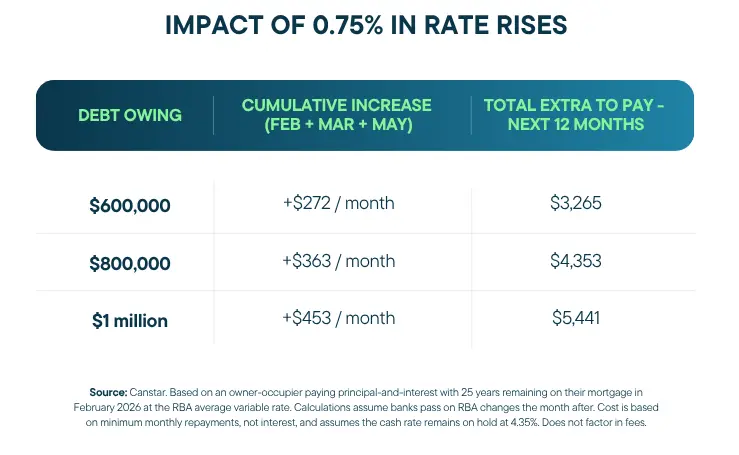

What the increases mean in dollars

According to Canstar analysis, a borrower with $600,000 remaining on their mortgage is now paying an extra $3,265 per year in repayments following the three increases.

For many households, that’s a meaningful change to monthly cash flow.

How borrowers are responding

Many borrowers are:

- Reviewing their loan rate and features.

- Refinancing to more competitive products.

- Tightening discretionary spending.

- Building buffers in offset or savings accounts.

Even small adjustments can help improve flexibility if repayments increase further.

Why planning matters

The Reserve Bank has made it clear that inflation remains a concern, and further rate increases are still possible.

That’s why many borrowers are now budgeting for repayments to rise again rather than assuming rates have peaked.

At Goodwill Finance, we can help you review your loan, compare what’s available across the market, and work through strategies to improve your position in the current environment.

Refinancing Activity Surges

Borrowers are clearly responding to rising rates – and refinancing is becoming one of the biggest mortgage trends in the market.

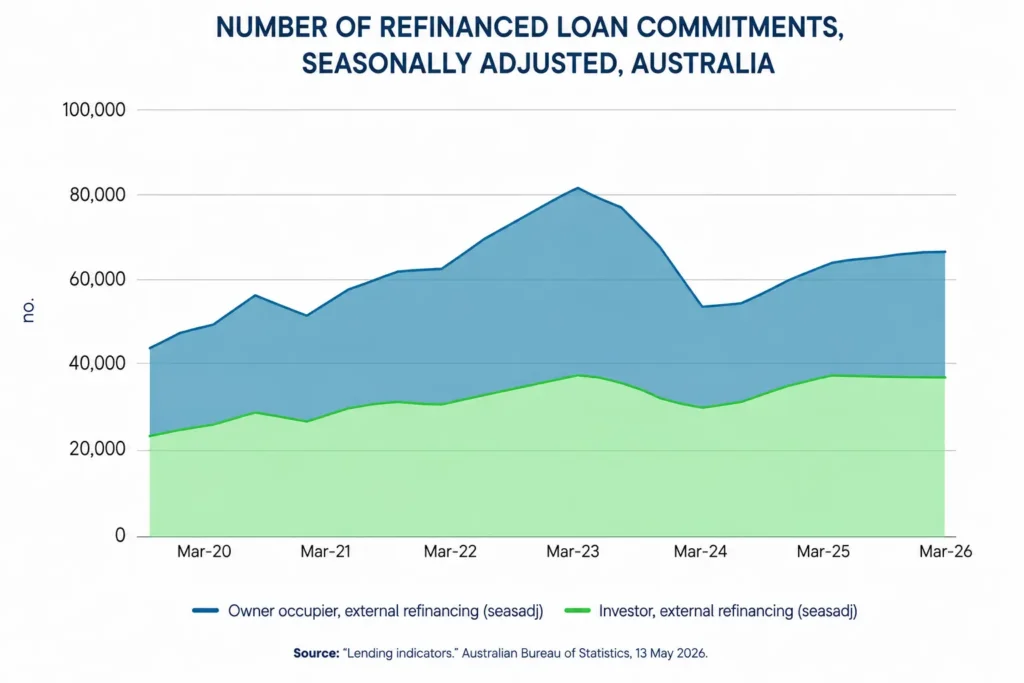

The latest ABS lending data shows refinancing activity jumped sharply in the March quarter, as borrowers reacted to the Reserve Bank’s February and March rate rises.

That trend may strengthen further once the May increase fully flows through.

The numbers tell the story

Compared to a year earlier:

- Owner-occupier refinancing rose 19.5%.

- Investor refinancing rose 3.3%.

- Total home loan commitments rose 8.6%.

But compared to the previous quarter, overall loan commitments fell 6.2%, suggesting some buyers may already be becoming more cautious.

Why timing matters here

This data captures the first two 2026 rate rises and the early stages of the Middle East conflict.

But it does not yet include the May rate rise and the federal Budget’s property tax changes – which means borrowing behaviour could shift again over the coming months.

Right now, many borrowers aren’t necessarily looking for the absolute lowest rate.

Instead, they’re thinking about:

- Managing higher repayments.

- Improving monthly cash flow.

- Creating more certainty if rates rise again.

That’s why refinancing conversations are increasing across the market.

We can help you compare your current loan against what’s available now and assess whether changing lenders, restructuring your loan, or improving your cash flow could make a difference.

New Fund Targets Housing Bottlenecks

One of the biggest barriers to new housing isn’t always construction – it’s infrastructure.

In many areas, housing projects are delayed because roads, water, sewerage and power connections aren’t ready.

To address that problem, the federal government announced a new $2 billion Local Infrastructure Fund in the Budget.

What the fund will do

The funding will help councils and utilities deliver the ‘last mile’ infrastructure needed to support new housing developments.

The government says the fund could support up to 65,000 homes over the next decade.

Why infrastructure matters for housing

The funding will only be available to states and territories that commit to reforms such as:

- Speeding up planning approvals.

- Making more land available.

- Simplifying building rules.

The government believes those changes could support more housing supply across Australia.

What it could mean for buyers

Housing supply has become a major affordability issue.

If more land and infrastructure become available, it could gradually improve housing choice and reduce some pressure on prices and rents.

Of course, these changes won’t happen overnight.

Over time, changes like these could influence where housing growth occurs and which areas see the biggest increase in supply.

As rates rise and new housing policies emerge, small financial decisions can have a bigger impact. If you’re thinking about refinancing, investing or buying, you can reach out to us at [email protected] or 0423 459 480, and we’ll explore your options.

Disclaimer: The information provided is of a general nature and does not take into account your personal financial circumstances, goals, or needs. It should not be considered financial or investment advice, nor a recommendation or invitation to acquire financial products or services. You should not act solely on this information without obtaining professional financial advice tailored to your situation. Any loan application is subject to a full assessment of your financial position, as well as the lender’s terms, conditions, fees, charges, and eligibility criteria.