The recent Reserve Bank decision isn’t the only big news. Here are four other stories that could influence your plans:

- The government scheme reshaping buyer behaviour

- What to know before building a home

- Electrified vehicles reach a new milestone

- Listings surge as buyers become cautious

The expansion of the 5% Deposit Scheme in October 2025 has had a big impact.

According to Equifax, lenders that participate in the scheme recorded a 16.4% increase in loan volumes between October 2025 and March 2026, while demand for non-participating lenders fell 6.5%.

At the same time, borrower enquiries increased 22.8% among 18–25-year-olds and 17.4% among 26–35-year-olds.

Why the scheme is attracting attention

Normally, buyers with less than a 20% deposit need to pay lenders mortgage insurance

(LMI).

Under the 5% Deposit Scheme, eligible buyers can purchase with as little as a 5% deposit without paying LMI, because the federal government guarantees part of the loan.

That can save thousands of dollars and help buyers enter the market sooner.

Buyers are broadening their search

Interestingly, Equifax found 81.9% of first home buyers purchased outside their existing suburb.

That suggests many buyers are prioritising affordability and opportunity over familiarity.

The trade-offs to consider

A smaller deposit can help you buy sooner.

But it also means:

- Borrowing more.

- Paying more interest over time.

- Having less equity initially.

Not sure whether the 5% Deposit Scheme is the right fit? We can help you explore your options and see what may be available.

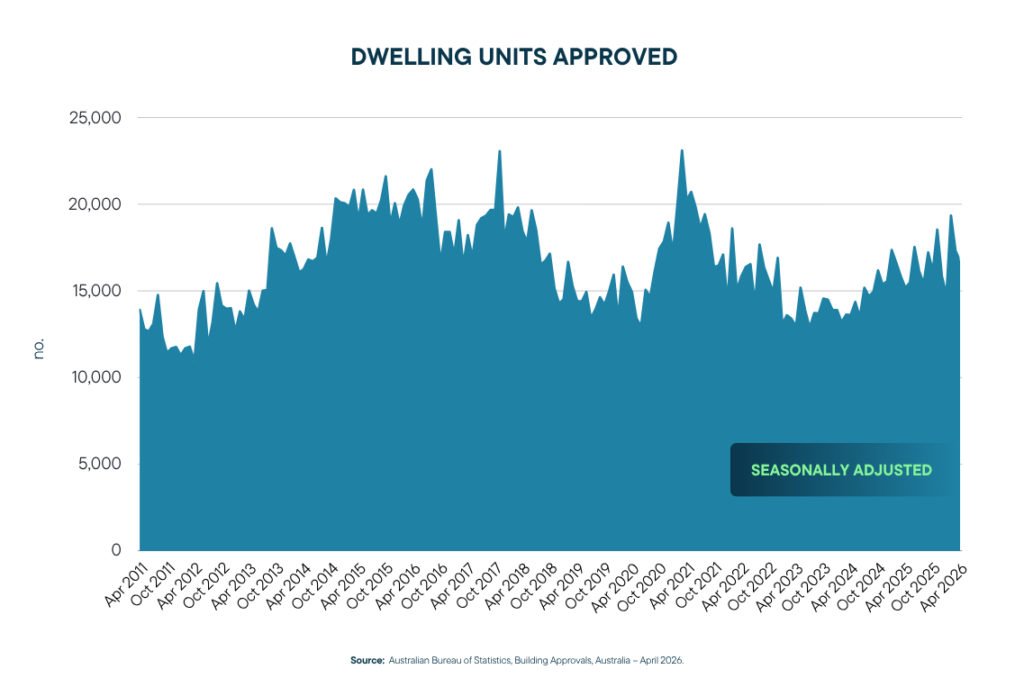

Building a home remains a popular option for Australians looking for more choice and newer housing, despite higher interest rates.

According to the ABS, 200,424 homebuilding approvals were issued in the year to April.

That’s 8.5% higher than the previous 12-month period.

While encouraging, it’s still below the pace needed to achieve the National Housing Accord target of building an average of 240,000 homes per year in the five years to June 2029.

How construction loans work

Construction loans differ from standard home loans.

Instead of receiving the full loan amount upfront, funds are generally released in stages as construction progresses.

Typical stages include:

- Slab or foundation.

- Frame.

- Lock-up.

- Fit-out.

- Completion.

During construction, borrowers often pay interest-only on the amount that’s been drawn down.

The realities of building a home

Building your own home can offer more choice over design and access to newer features and greater energy efficiency.

However, it can also involve delays, variations and unexpected costs.

Before you sign a building contract, it’s worth understanding how construction finance works and what you may be able to borrow.

Electric vehicles are moving from niche to mainstream, with a record number of Australians choosing electrified cars.

According to VFACTS data, 20% of all new vehicles sold in May were battery electric vehicles, while 46% were electrified vehicles when hybrids and plug-in hybrids are included.

That’s the highest share on record.

Rising fuel costs, expanding model choice and government incentives have all helped push EV adoption higher.

The cost equation is changing

Generally:

- EVs cost more upfront – but often cost less to run and maintain.

- Traditional vehicles are usually cheaper to buy – but often have higher ongoing fuel costs.

The right option depends on how long you expect to keep the vehicle and how much you drive.

Questions worth asking

Before making a decision, consider:

- Your budget.

- Charging availability.

- Expected annual kilometres.

- Servicing and running costs.

- Resale value.

For some households, an EV may save money over the long term. For others, a traditional vehicle may still be the better fit.

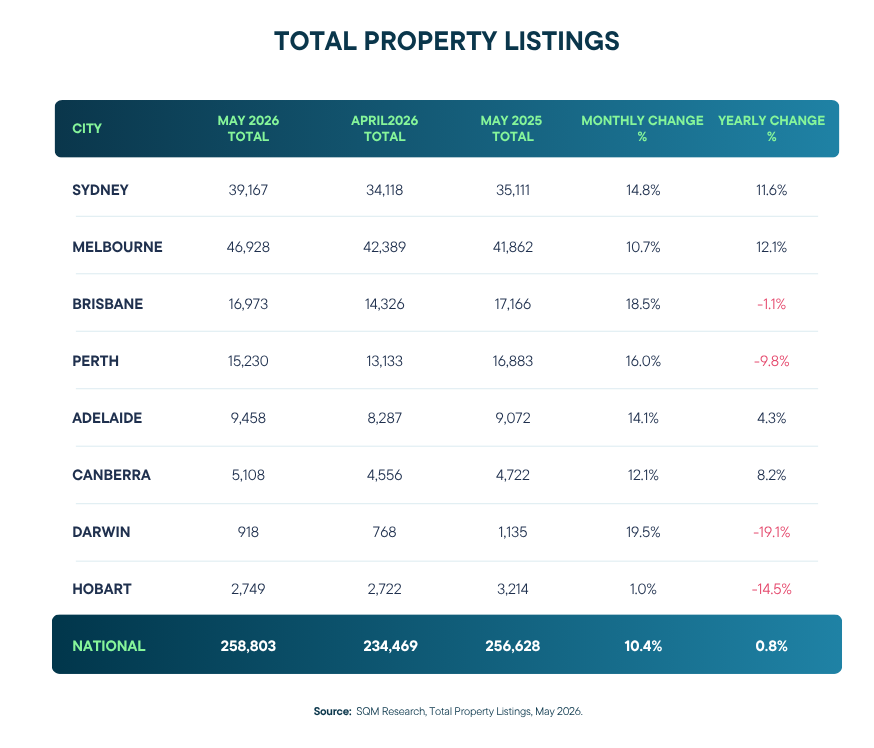

Buyers are getting more choice as housing supply increases – but the reasons behind the rise in listings are worth understanding.

According to SQM Research, total residential listings across Australia in May were 10.4% higher than April.

That included a 5.0% increase in new listings. Older listings also increased 10.5%, suggesting some properties are taking longer to sell.

Why the market is cooling

Several factors are weighing on buyer demand:

- Higher interest rates.

- Stretched affordability.

- Global economic uncertainty.

- Lower consumer confidence.

As a result, homes are generally taking longer to sell and buyers are becoming more selective.

What it means for buyers and sellers

For buyers, a cooling market can create:

- More choice.

- Less competition.

- Greater negotiating power.

For sellers, it can mean:

- Longer selling campaigns.

- More competition from other listings.

- Greater importance of realistic pricing.

Importantly, a cooling market is not the same as a collapsing market.

Property prices remain well above pre-pandemic levels and conditions continue to vary significantly between locations.

More choice in the market can create new opportunities for buyers, but preparation still matters. Knowing your borrowing capacity can help you act when the right property comes along.

From 5% deposits to building finance and vehicle choices, the latest trends show how quickly conditions are changing. If you’d like to plan your finances for your property purchase, we are more than happy to help. You can reach out to us at [email protected] or 0423 459 480.

Disclaimer: The information provided is of a general nature and does not take into account your personal financial circumstances, goals, or needs. It should not be considered financial or investment advice, nor a recommendation or invitation to acquire financial products or services. You should not act solely on this information without obtaining professional financial advice tailored to your situation. Any loan application is subject to a full assessment of your financial position, as well as the lender’s terms, conditions, fees, charges, and eligibility criteria.