From interest rate uncertainty to new ways first home buyers are entering the market, several shifts are reshaping property decisions. These four trends could influence your next move.

- Rate rise reshapes the market

- How the 5% Deposit Scheme is changing buying

- Fixed or variable – which is right for you?

- Building a home is back on the radar

Find out more below.

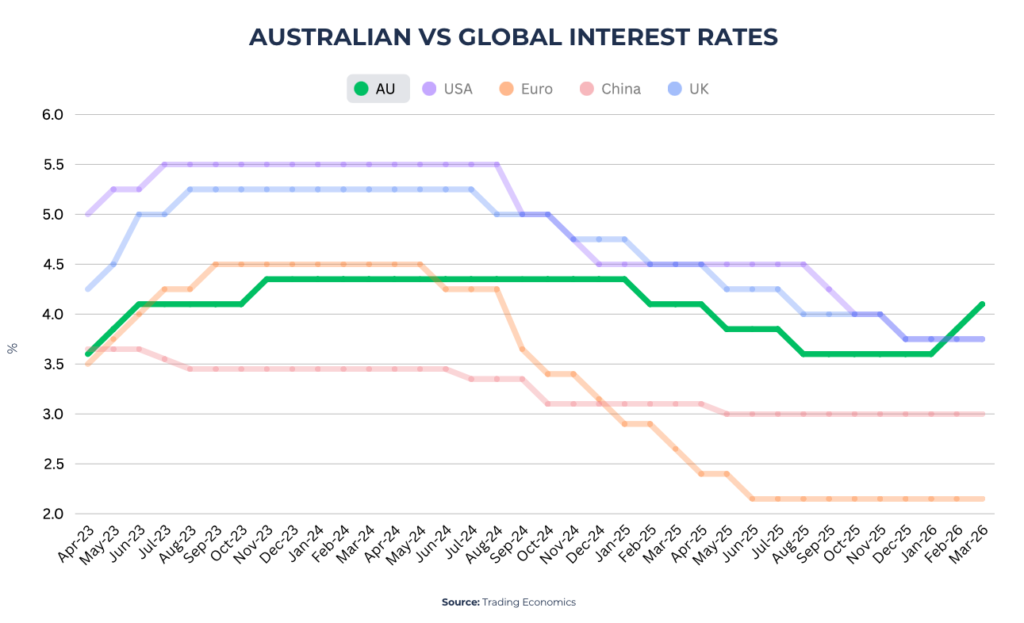

Over the past week, lenders have been passing on the full 0.25-percentage-point increase to borrowers, with repayments now lifting across the market.

This comes on top of the February move, so for many households, rates have now increased twice in a short period – putting additional pressure on monthly budgets.

Globally, interest rates remain elevated, with Australia continuing to move in line with broader trends across major economies.

Fixed rates have been moving higher in recent weeks as markets have already priced in further expected rate increases – we’ve covered this in more detail in a story below.

What to watch next

With rates moving again, attention now shifts to what comes next.

Economists are watching inflation, labour market conditions and global pressures. These will shape whether rates hold, rise further or begin to ease.

With repayments now adjusting, this is typically where small differences between loans start to matter more, making this a useful time to check whether your current rate and structure are still competitive.

More buyers are entering the market sooner – even as interest rates rise.

New data from banking regulator APRA shows a sharp increase in buyers purchasing with smaller deposits.

The share of owner-occupier loans with a deposit of 5% or less rose 59.8% over the year to December 2025.

That shift closely follows the federal government’s expansion of the 5% Deposit Scheme in October 2025.

Even after the recent rate rise, demand remains strong – suggesting many buyers are still confident about entering the market.

Why this is happening

The scheme allows eligible buyers to purchase with just a 5% deposit without paying lenders mortgage insurance (LMI).

For many first home buyers, avoiding LMI can mean saving tens of thousands of dollars.

Instead of waiting years to save a full 20% deposit, some buyers are choosing to enter the market sooner.

More buyers are also looking at affordable or regional areas, where borrowing capacity can stretch further in a higher-rate environment.

What this means for buyers

This isn’t just a statistic – it’s a practical pathway.

But eligibility rules, lender participation and loan structure all matter.

Getting those details right can make a significant difference.

Goodwill Finance can help you understand how the scheme works, check your eligibility and structure the loan to suit your situation.

Fixed home loan rates have been repriced across lenders in recent weeks, with many moving higher ahead of the March rate rise as markets anticipated further increases.

One clear change – sub-5% fixed rates have largely disappeared, with most offers now sitting higher as funding costs have risen.

Behind this, bond yields have been trending upward, reflecting expectations that interest rates may stay elevated for longer.

Fixed rates don’t move directly with the RBA cash rate – they’re driven more by funding costs and bond yields, which reflect where markets expect interest rates to go next.

What’s happening across loan terms

- Shorter-term fixed (1–2 years) has moved more noticeably, tracking near-term rate expectations.

- Longer-term fixed (3–5 years) has been steadier, but has still gradually repriced higher.

- Fixed rates are increasingly being set based on where markets expect rates to go, not where they are today.

What this means now

Fixed rates are less about chasing a lower rate and more about certainty and planning.

That’s why some borrowers are now focusing more on loan structure, not just headline pricing.

At Goodwill Finance, we can help you compare fixed, variable and split options and structure your loan around your plans in the current environment.

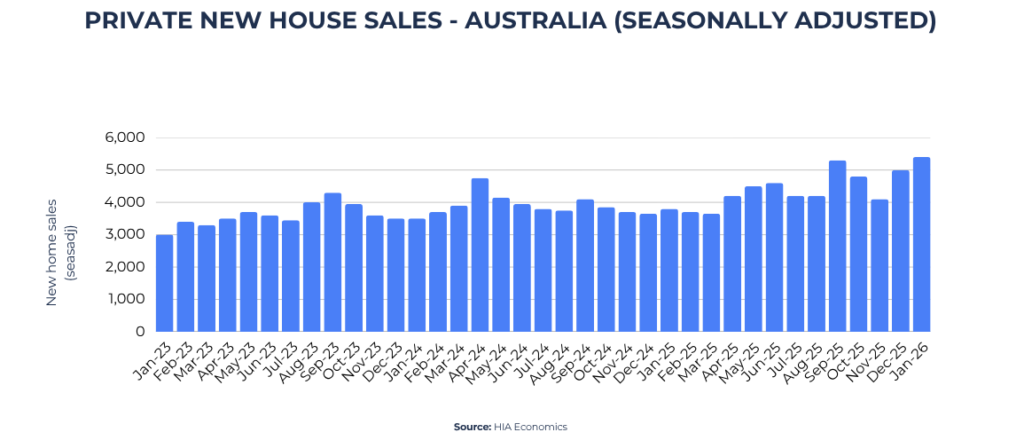

More buyers are turning to new builds as population growth lifts established home prices.

New home sales in the January 2026 quarter were 26.2% higher than a year earlier, according to the Housing Industry Association.

One key reason is demand.

Australia’s strong population growth has pushed up prices in the established housing market. That’s making it harder for some buyers to find affordable options.

For many households, building a new home has become an alternative entry strategy.

How construction finance works

Financing a new build is different from buying an existing home.

Instead of receiving the full loan at settlement, the lender releases funds in stages as the construction progresses.

These stages typically include:

- slab or foundation

- frame

- lock-up

- fit-out

- completion

During construction, borrowers usually pay interest-only on the funds already drawn down, which can help manage cash flow while the home is being built.

New builds may also come with grants, incentives or stamp duty concessions depending on where you buy.

Construction loans follow a different process from standard mortgages, so it helps to plan ahead before signing a building contract.

Want to talk through how the financing works and what lenders typically require? We are more than happy to help.

Between the latest interest rate developments, new opportunities for buyers with smaller deposits and stronger demand for new homes, the property landscape is shifting again. If you’re planning your next move, reach out and we’ll guide you through your options. Give us a call at 0423 459 480 or email us at [email protected].

Disclaimer: The information provided is of a general nature and does not take into account your personal financial circumstances, goals, or needs. It should not be considered financial or investment advice, nor a recommendation or invitation to acquire financial products or services. You should not act solely on this information without obtaining professional financial advice tailored to your situation. Any loan application is subject to a full assessment of your financial position, as well as the lender’s terms, conditions, fees, charges, and eligibility criteria.