With the next Reserve Bank decision on May 5 approaching, borrowers are reassessing their position. Here are four trends shaping rates, property prices and your options right now:

- The refinancing question more borrowers are asking

- How to get more value from your offset account

- Why property prices haven’t been falling

- A realistic path from renting to owning

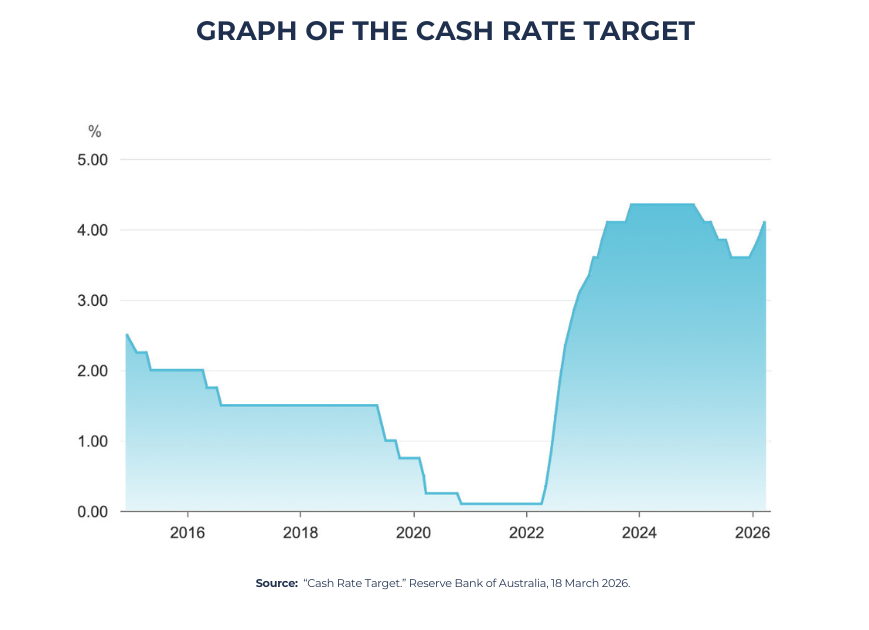

How To Stay Ahead As Rates Move Higher

Between the Middle East conflict, rising prices and two rate increases this year, many households are feeling the squeeze.

That’s why a lot of borrowers are reviewing their loan, not just riding it out.

Refinancing can help you:

- Secure a more competitive rate.

- Restructure your loan to suit current conditions.

- Improve cash flow.

But timing is the tricky part.

Refinance now or wait?

Refinancing now could mean reducing repayments sooner and getting ahead of further rate rises.

Waiting could mean accessing better rates if markets settle and avoiding switching costs too early.

There’s no perfect moment – it depends on your situation, not just the market.

Where to start

The key is understanding what your current loan looks like compared to what’s available now.

Your mortgage broker can help you review your rate, compare options and decide whether acting now or waiting makes more sense for you.

Your Offset Could Be Doing More

As rates rise, offset accounts are becoming more important than many people realise.

That’s because an offset account reduces the interest charged on your loan.

If, say, you have $700,000 outstanding on your loan and $40,000 in offset, you pay interest on only $660,000 (i.e. $700k minus $40k).

This is a hypothetical example – your situation may differ – that shows the power of offset.

As rates rise, the benefit compounds

As rates rise, the interest saved on that hypothetical $40,000 increases.

That means:

- Stronger savings without changing your repayments.

- Faster loan reduction over time.

- Better use of your cash than standard savings.

Making it work properly

Not all offset setups are equal.

Things like account structure, cash flow and loan features can make a big difference.

Your mortgage broker can help you review how your offset is set up and whether it’s working as effectively as it could in the current environment.

What’s Really Driving Property Prices

Rising rates haven’t automatically led to falling property prices – and supply is a big reason why.

It’s easy to assume higher rates mean lower prices.

But the data tells a more complex story.

What’s happening now

- National prices rose 0.7% in March (source: Cotality).

- New listings increased 3.8% month-on-month (SQM Research).

- But total listings are still 6.7% lower than a year ago.

That means supply is improving slightly – but still tight overall.

The bigger constraint

New construction isn’t keeping up.

Master Builders Australia has lowered its forecast for the amount of homes built over the five-year period of the National Housing Accord.

The reason? Labour shortages and cost pressures are slowing supply.

Property prices are being supported by:

- Limited housing supply.

- Ongoing population growth.

- Constrained construction.

So while growth may slow, a broad price decline isn’t guaranteed.

Your mortgage broker can help you assess what this means for your borrowing power and whether now is the right time to act.

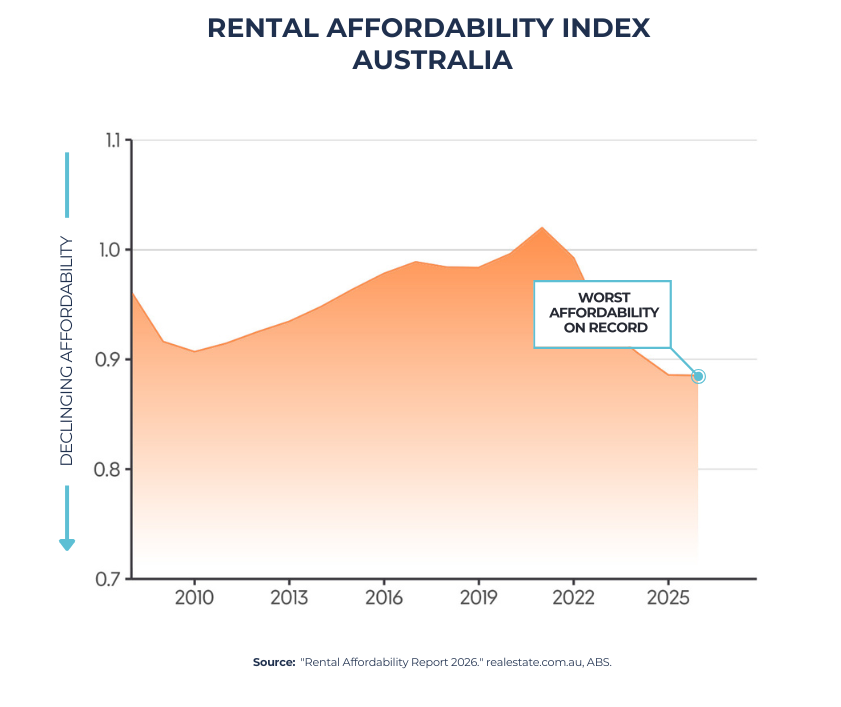

Rental Affordability Hits New Low

Rents are rising faster than wages. That’s making the path to buying harder – but not impossible.

Rental affordability is now at its lowest level since at least 2008, according to realestate.com.au.

That’s putting pressure on renters trying to save.

Why it feels harder

Many people are juggling rising rents, higher living costs, elevated property prices and rising interest rates.

It’s a tough combination.

That’s why many buyers are adjusting their approach, rather than waiting for perfect conditions.

That could mean buying a more affordable property, looking at different locations, exploring strategies like rentvesting or using government support schemes where eligible.

The shift that changes timelines

The biggest shift is moving from ‘just waiting’ to understanding what’s possible now.

Even if you’re not ready yet, knowing your borrowing capacity and options can change your timeline.

Contact a mortgage broker if you want a realistic path based on your income, savings and goals.

As rates move, rents climb and buyers adjust their approach, staying proactive can make a real difference. If you’re thinking about refinancing or buying, you can contact Goodwill Finance by calling us at 0423 459 480 or emailing us at [email protected] and look at your next step.

Disclaimer: The information provided is of a general nature and does not take into account your personal financial circumstances, goals, or needs. It should not be considered financial or investment advice, nor a recommendation or invitation to acquire financial products or services. You should not act solely on this information without obtaining professional financial advice tailored to your situation. Any loan application is subject to a full assessment of your financial position, as well as the lender’s terms, conditions, fees, charges, and eligibility criteria.